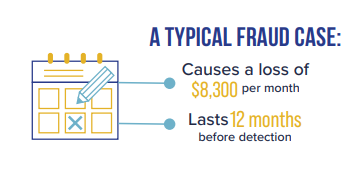

Fraud Detection is vital to a school district. According to the latest report from the Association of Certified Fraud Examiners (ACFE), a single, ongoing fraud case causes a loss of $8,300 per month and lasts an average of 12 months before it is discovered. This equates to an annual loss of $99,600. For a school district, that is almost the salary of two full-time teachers. Annually, the ACFE states an organization loses between 5-7% of their revenue to fraud. In a time of high inflation and shrinking budgets and enrollments, the impact of a fraud costs districts immensely. Fraud needs to be uncovered and stopped in the most timely manner possible. There are four main ways for a school district to detect an ongoing fraud. These are fraud hotlines, data analytics, external auditors, and internal auditors.

The number one method for a school district to detect fraud is through the use of a fraud hotline. A fraud hotline is a way for stakeholders of a district (employees, parents, students, vendors) to safely and anonymously report suspected cases of fraud, waste, and abuse. According to the ACFE, utilizing a fraud hotline reduces the time for a fraud to be detected from 18 months to 12. It also reduces the median loss from that fraud from $200,000 to $100,000. At a minimum a school district must have some sort of fraud reporting mechanism to mitigate the impact of fraud.

A second way that fraud is detected is through the use of data analytics. In a nutshell, data analytics is examining school district financial transactions looking for outliers or abnormal trends. One data analytics technique is horizontal analysis. In horizontal analysis, you could examine the cost of teacher professional development for the last five years. If in the first four years, your district spent $100,000 on professional development each year and in year five it spent $200,000, that would be an outlier and require further examination. This same technique could be used for travel expenses, mileage reimbursement, expense reimbursement, and spending per vendor. Horizontal analysis is just one of many data analytical techniques, more will be discussed in future posts.

The last two methods of fraud detection are the utilization of external and internal auditors. External auditors typically are not looking for fraud at your district. There main concern is making sure your financial statements accurately reflect your district’s true financial position. However, they are required to take into account the possibility of fraud in the planning of their engagement. Internal auditors, if your district has them, are often tasked with investigating fraud (if detected) and may come across fraud during an audit they are performing. In addition, internal auditors often conduct an annual district wide fraud risk assessment, which directs their annual audit plan.

All four methods of fraud detection mentioned in this article will be examined closer in upcoming posts. These methods are the foundation for administrators, teachers, board members, and other stakeholders to mitigate the impact of fraud on your district by uncovering it as soon as possible. EduFraud is developing tools and trainings to help your district detect fraud that may be happening at your school district. Please come back to this site for future posts that will help you protect your district’s assets and reputation.